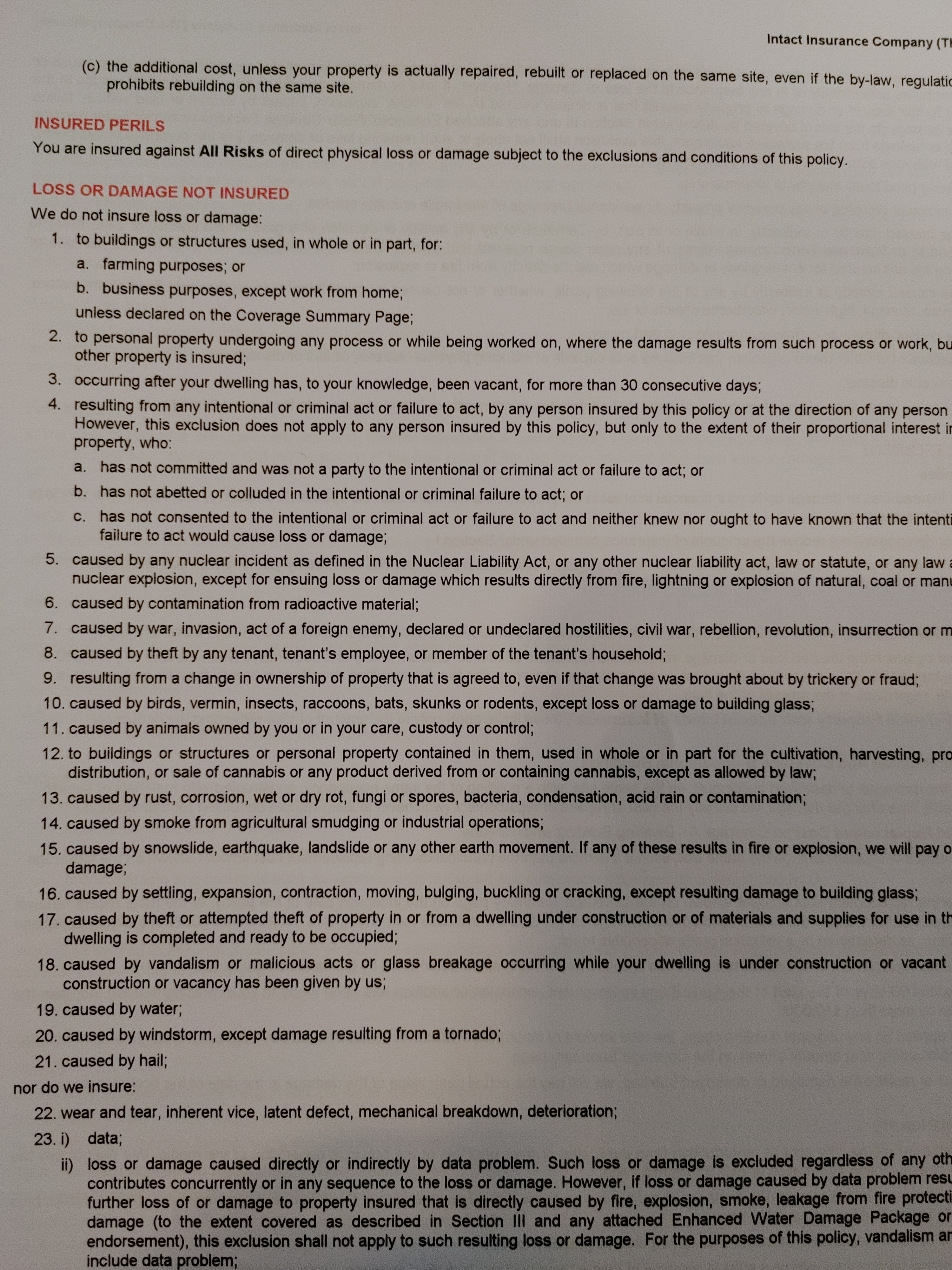

This is plausible. That or it’s just a really cheap policy - no windstorm/hail damage is very much NOT normal for homeowners though, even so.

The rest of this is pretty standard stuff and the fact that people seem angry/surprised by it speaks volumes to how little attention they’ve paid to their own policies. Read your paperwork y’all. It’s tedious, but you are also party to the insurance contract that you’re paying for. It can also help you find grey areas of coverage, and a grey area (ambiguous language) tends to work out well for the insured party (you, if you have insurance).

Right. Barring some weird oceanfront property in Florida where you’re looking at buying separate flood insurance. And you can bet that your mortgage lender will want you to have that.

{kind=link}

Is this for a renter of somebody else’s property? Barring the damaged by water part and maybe the vermin it seems pretty standard.

E.g. if an upstairs apartments floods I’d want my insurance to cover my belongings while the landlord’s insurance would cover the building.

That seems the most likely damage (even more than fire, etc) that I’d want to have covered by insurance as a renter.

Of course I just glanced at it so please let me know if there’s anything I missed.

This is plausible. That or it’s just a really cheap policy - no windstorm/hail damage is very much NOT normal for homeowners though, even so.

The rest of this is pretty standard stuff and the fact that people seem angry/surprised by it speaks volumes to how little attention they’ve paid to their own policies. Read your paperwork y’all. It’s tedious, but you are also party to the insurance contract that you’re paying for. It can also help you find grey areas of coverage, and a grey area (ambiguous language) tends to work out well for the insured party (you, if you have insurance).

Right. Barring some weird oceanfront property in Florida where you’re looking at buying separate flood insurance. And you can bet that your mortgage lender will want you to have that.