The chart is for household income. With each generation, there’s an increase in the percentage of the generation living at home. This is noted in the paper, but not in The Economist article. We’ll see if Gen Z makes the switch like Millennials were during their 30s.

A couple of asides. The Economist graph isn’t very easily matched with one from the paper. There are several graphs that share similar contours, but The Economist has changed the aspect ratio enough that it’s hard to identify with visual inspection. Most curious, though, is The Economist’s choice of starting the x-axis at 15 years old. All the graphs in the paper start at 20myesrs old.

The conclusion in The Economist piece is as follows:

What does this wealth mean? It can seem as if millennials grew up thinking a job was a privilege, and acted accordingly. They are deferential to bosses and eager to please. Zoomers, by contrast, have grown up believing that a job is basically a right, meaning they have a different attitude to work. Last year Gen Z-ers boasted about “quiet quitting”, where they put in just enough effort not to be fired. Others talk of “bare minimum Monday”. The “girlboss” archetype, who seeks to wrestle corporate control away from domineering men, appeals to millennial women. Gen Z ones are more likely to discuss the idea of being “snail girls”, who take things slowly and prioritise self-care.

It is clear that The Economist has an agenda of dividing Millennials and Gen Z. The paper makes no claims about Gen Z and their economic outlook. The data is simply not there. Rather, The Economist is recapitulating tired themes of “the youth these days” and “kids don’t want to work”.

People work when they have something to work towards, with and for people they care about. People work hard because it fills us with meaning purpose. When we are young, we do and should be creating relationships and learning about ourselves, the world, who we wish to be in the world, and who we wish to journey with.

I forever will call bullshit on the anti-youth themes of our culture. It dimishes it and serves only the most well established and crumudgenly amongst us. Articles like these have all too obvious subtext of “shut up, work hard, and grow up”.

Living at home doesn’t necessarily make you part is the same household. When I started paying for my dad’s electrical bills and he stopped filing me as a dependent, we became roommates, not part of the same household.

Missing some really important variables, there (inflation, buying power, etc)… while using metrics that present an a deliberately inaccurate picture (median rather than average, and not adjusted for outliers).

Basically, this chart is useless, deceptive propaganda.

If it used the mean you’d complain about that too, since it’s higher than the median. The median already completely throws out any outliers. That’s why it’s lower than the median because the distribution is right skew

And people can’t afford houses, college, healthcare, etc. because…? Like cool chart, but my generation will literally never be as financially stable as those who came before. I guess it’s fun to pretend we’re better off than we are though.

Imagine paying for college with your income rather than loans.

People can afford more things now than the previous generation

There are things that increased in price faster, like college. But that’s offset by other things that didn’t increase as fast, like fuel. There are other things that got cheaper, like computers and phones. You’re cherry picking the things that got more expensive, but those are not 100% of a person’s expenses

You’re missing the whole point. Think about it another way: You listed things that go down in value or get used up. They listed things that appreciate in value and build wealth.

You’re comparing (barely) being able to afford the cheap iPhones and gas to an education and homeownership.

Those things still cost money and you still need them.

If food prices didn’t go up as fast as housing, and you say “housing builds wealth and food gets used up” which is true, but you need to eat to live. Food not going up so fast is a good thing.

Housing building wealth is a bad thing. Houses should go down in value, we should be building so many that old houses should be worth less than me ones, like they do in Japan

Yeah and look 2 years back on your same graph and see the big 11% in one month.

And let’s not forget that this is multiplicative. So these months/years with high inflation are still felt today even if the inflation is relatively normal.

But you are disingenuous in your arguments, while accusing others of doing that same thing.

If the food cost follows the inflation and the inflation is 20%, will you say that food prices are ok because they follow inflation?

It would be fine if the wage followed the same inflation as food and housing, but the reality is that wage lag and stagnate behind inflation.

So yeah, if your groceries cost you 20% and you haven’t received an equivalent wage increase, then your groceries cost significantly more in absolute term because you still have the same money as before, but your food cost more for the same grocery basket you bought before inflation.

But again, you are disingenuous, so probably just a troll. I won’t respond anymore.

It doesn’t account for things like the median home price in 1950 being ~$7000 vs over $400,000 today. The chart doesn’t show a peak earning increase of 10x between the Silent Generation vs GenX, which seems to have done the best, albeit only briefly. Adjusting the average home price for CPI makes a ‘50s $7k home less than $100k today.

So you are saying that Millenials at their peak now are making as much as Boomers did 20 years ago when houses were about a quarter of the price, and somehow your conclusion is that Millenials are doing great? Or let’s look at age vs age: at age 40 a Millenial makes twice as much as a Boomer did at that age, but a Boomer at age 40 could buy a new house in a nice suburb for under $100k when that exact same house is over $300k now.

The CPI used for that doesn’t distinguish between generations so the lower house prices from people who got their houses in the 1990s are going to be mixed with the higher house prices of those trying to get their houses now with the former dilluting the latter.

Further the inflation index doesn’t reflect a lowering utility value of houses: if dwellings further and furthe taway from the places of work are built and occupied because people are been pushed further out by higher prices, so the utility of the houeses is lowet, that is not reflected in the CPI (at most it makes it a bit lower than it should be since the expanding pool of lower utility houses pulls the average price down a bit).

Further, as others pointed out, younger people are staying in their parents for longer and longer AND delaying childbirth, so their available income is higher because they’re not spending any money in housing or children.

The numbers not only do not reflect a better life, they’re not even comparable in their own merits across generations because the personal inflation of somebody looking for a place to live now is totally different from the one of those who have been living in a house they bought 30 years ago.

That’s a valid criticism, but most mortgages are 30 years, so anyone who bought a house in 1994 is paying their last payments on it.

People like my dad who bought houses during the 2000s didn’t get a good deal. Sure, it still eventually appreciated, but it’s not an outrageously good deal compared to getting a house just a few years later

That said, it’s getting better in places that build new housing

Sure, but inflation doesn’t factor in price hikes, for instance medical insurance, drug prices, house prices, rent, collage tuition or new expenditures that didn’t exist 20 years ago. These don’t follow the curve of inflation, they are artificialy inflated which is shown in increased profit margins.

Dude, I’m not complaining I’m giving you examples of things that they don’t account for. Rent is different, you have landlords jacking the price to an extreme, and then you have those who follow the inflation curve. It’s just dishonest.

It looks like there’s nothing I can say to make you see, but even accounting for inflation, the cost of living has been outpacing wages for decades! That’s why the average US worker in the 1950s could support a home with their wages alone, but today, two people working full-time jobs still can’t afford a home.

That’s because the cost of living has been outpacing wages.

You’re deliberately ignoring what I actually wrote. Two high school grads working minimum wage jobs in 1960 could have been homeowners in about five years. There are hundreds of reasons why the ownership rate was lower in the past.

I wonder what happens to this chart if you remove the top 1% from the calculations. “Median” basically means halfway between the top and bottom… The massive and increasing wealth gap means this graph is basically worthless.

Oh I thought it was because they like Trump, are Russian bots, and tankies. At least if people here are to be believed.

Each successive generation has a higher income even accounting for inflation

Sure Bud, nice meaningless chart.

I’m not your Bud, friend

Your use of ancient reddit memes doesn’t make your chart meaningful.

It’s a South Park quote, nothing to do with Reddit

Here’s the source for that chart. And the paper for that chart.

The chart is for household income. With each generation, there’s an increase in the percentage of the generation living at home. This is noted in the paper, but not in The Economist article. We’ll see if Gen Z makes the switch like Millennials were during their 30s.

A couple of asides. The Economist graph isn’t very easily matched with one from the paper. There are several graphs that share similar contours, but The Economist has changed the aspect ratio enough that it’s hard to identify with visual inspection. Most curious, though, is The Economist’s choice of starting the x-axis at 15 years old. All the graphs in the paper start at 20myesrs old.

The conclusion in The Economist piece is as follows:

It is clear that The Economist has an agenda of dividing Millennials and Gen Z. The paper makes no claims about Gen Z and their economic outlook. The data is simply not there. Rather, The Economist is recapitulating tired themes of “the youth these days” and “kids don’t want to work”.

People work when they have something to work towards, with and for people they care about. People work hard because it fills us with meaning purpose. When we are young, we do and should be creating relationships and learning about ourselves, the world, who we wish to be in the world, and who we wish to journey with.

I forever will call bullshit on the anti-youth themes of our culture. It dimishes it and serves only the most well established and crumudgenly amongst us. Articles like these have all too obvious subtext of “shut up, work hard, and grow up”.

Fuck that noise.

Living at home doesn’t necessarily make you part is the same household. When I started paying for my dad’s electrical bills and he stopped filing me as a dependent, we became roommates, not part of the same household.

Missing some really important variables, there (inflation, buying power, etc)… while using metrics that present an a deliberately inaccurate picture (median rather than average, and not adjusted for outliers).

Basically, this chart is useless, deceptive propaganda.

It’s inflation adjusted

If it used the mean you’d complain about that too, since it’s higher than the median. The median already completely throws out any outliers. That’s why it’s lower than the median because the distribution is right skew

And people can’t afford houses, college, healthcare, etc. because…? Like cool chart, but my generation will literally never be as financially stable as those who came before. I guess it’s fun to pretend we’re better off than we are though.

Imagine paying for college with your income rather than loans.

People can afford more things now than the previous generation

There are things that increased in price faster, like college. But that’s offset by other things that didn’t increase as fast, like fuel. There are other things that got cheaper, like computers and phones. You’re cherry picking the things that got more expensive, but those are not 100% of a person’s expenses

You’re missing the whole point. Think about it another way: You listed things that go down in value or get used up. They listed things that appreciate in value and build wealth.

You’re comparing (barely) being able to afford the cheap iPhones and gas to an education and homeownership.

Those things still cost money and you still need them.

If food prices didn’t go up as fast as housing, and you say “housing builds wealth and food gets used up” which is true, but you need to eat to live. Food not going up so fast is a good thing.

Housing building wealth is a bad thing. Houses should go down in value, we should be building so many that old houses should be worth less than me ones, like they do in Japan

It’s fun that tvs and computers got cheaper, but housing and food are through the roof.

It’s cool that I can buy a laptop for 500$ dollars, but it’s a one time purchase that we can live without.

Food is not through the roof

https://tradingeconomics.com/united-states/food-inflation

2.2% vs. the previous year

Yeah and look 2 years back on your same graph and see the big 11% in one month.

And let’s not forget that this is multiplicative. So these months/years with high inflation are still felt today even if the inflation is relatively normal.

But you are disingenuous in your arguments, while accusing others of doing that same thing.

So kindly fuck off

That’s in line with the inflation numbers. Food costs did not outpace inflation in any significant way

If the food cost follows the inflation and the inflation is 20%, will you say that food prices are ok because they follow inflation?

It would be fine if the wage followed the same inflation as food and housing, but the reality is that wage lag and stagnate behind inflation.

So yeah, if your groceries cost you 20% and you haven’t received an equivalent wage increase, then your groceries cost significantly more in absolute term because you still have the same money as before, but your food cost more for the same grocery basket you bought before inflation.

But again, you are disingenuous, so probably just a troll. I won’t respond anymore.

Meaningless chart.

It doesn’t account for things like the median home price in 1950 being ~$7000 vs over $400,000 today. The chart doesn’t show a peak earning increase of 10x between the Silent Generation vs GenX, which seems to have done the best, albeit only briefly. Adjusting the average home price for CPI makes a ‘50s $7k home less than $100k today.

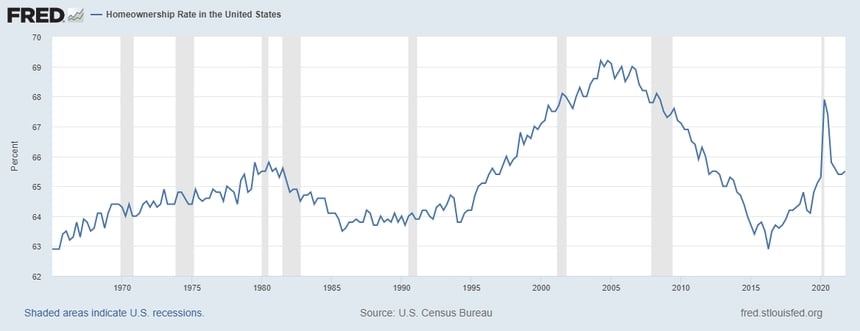

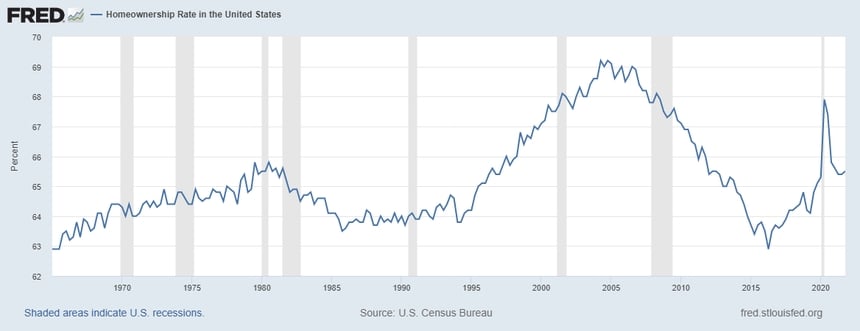

Home ownership right now is still pretty high

Just because it was cheaper doesn’t mean people could afford them

So you are saying that Millenials at their peak now are making as much as Boomers did 20 years ago when houses were about a quarter of the price, and somehow your conclusion is that Millenials are doing great? Or let’s look at age vs age: at age 40 a Millenial makes twice as much as a Boomer did at that age, but a Boomer at age 40 could buy a new house in a nice suburb for under $100k when that exact same house is over $300k now.

The chart is indexed for inflation. Housing went up faster, but things like fuel are not so expensive comparatively

You’re cherry picking things that went up faster

By the way, home ownership rate:

It’s not lower now

The CPI used for that doesn’t distinguish between generations so the lower house prices from people who got their houses in the 1990s are going to be mixed with the higher house prices of those trying to get their houses now with the former dilluting the latter.

Further the inflation index doesn’t reflect a lowering utility value of houses: if dwellings further and furthe taway from the places of work are built and occupied because people are been pushed further out by higher prices, so the utility of the houeses is lowet, that is not reflected in the CPI (at most it makes it a bit lower than it should be since the expanding pool of lower utility houses pulls the average price down a bit).

Further, as others pointed out, younger people are staying in their parents for longer and longer AND delaying childbirth, so their available income is higher because they’re not spending any money in housing or children.

The numbers not only do not reflect a better life, they’re not even comparable in their own merits across generations because the personal inflation of somebody looking for a place to live now is totally different from the one of those who have been living in a house they bought 30 years ago.

That’s a valid criticism, but most mortgages are 30 years, so anyone who bought a house in 1994 is paying their last payments on it.

People like my dad who bought houses during the 2000s didn’t get a good deal. Sure, it still eventually appreciated, but it’s not an outrageously good deal compared to getting a house just a few years later

That said, it’s getting better in places that build new housing

Yeah but it doesn’t tell the whole truth, cost of living has been rising steadily as well.

Cost of living is inflation, which this chart takes into account

Sure, but inflation doesn’t factor in price hikes, for instance medical insurance, drug prices, house prices, rent, collage tuition or new expenditures that didn’t exist 20 years ago. These don’t follow the curve of inflation, they are artificialy inflated which is shown in increased profit margins.

Rent is literally a third of inflation calculation

How do you complain it doesn’t factor it when it’s the biggest contributor?

Dude, I’m not complaining I’m giving you examples of things that they don’t account for. Rent is different, you have landlords jacking the price to an extreme, and then you have those who follow the inflation curve. It’s just dishonest.

That list is wrong because they do account for those things

You were proven wrong by another user, you’ve linked a graph with no sources or explanation.wjatvdo you expect?

That chart lacks context. The cost of living has drastically increased with each generation as well, far outpacing the increase in wages.

The cost of living is tracked by inflation, that’s what inflation is

It looks like there’s nothing I can say to make you see, but even accounting for inflation, the cost of living has been outpacing wages for decades! That’s why the average US worker in the 1950s could support a home with their wages alone, but today, two people working full-time jobs still can’t afford a home.

That’s because the cost of living has been outpacing wages.

But that’s only true in the 1970s and 1980s. In recent years wages have outpaced inflation

Why is home ownership now higher than before?

In 1960, minimum wage was $1.00/hour and the price of the average US home was $11,000.00

How many minimum wage workers are out there right now looking to buy a new home?

They weren’t buying then either

So, you agree, people were able to buy a house on minimum wage in the past and can’t do that today?

They were not, look at ownership rate.

You’re deliberately ignoring what I actually wrote. Two high school grads working minimum wage jobs in 1960 could have been homeowners in about five years. There are hundreds of reasons why the ownership rate was lower in the past.

Could have been, but did not buy homes. Explain why

If you actually had an argument, you’d be able to present a variety of proof, instead of just posting the same graph over and over.

Okay now do one that shows how much is available after paying for things like rent, food, car, etc.

Meaningless chart

That’s been done too

https://home.treasury.gov/news/featured-stories/the-purchasing-power-of-american-households

Purchasing power of American households is at all time high

Okay, now why hasn’t the minimum wage been raised in literal decades?

Honestly it just seems like you’re being obtuse

That’s the federal minimum wage, cities have certainly raised their own minimum wages

That’s why only like 1% of workers make the federal minimum wage

Nice cherry picking, you got any other fallacies to throw in there?

1% of workers is not very impactful for the average income

The workers who make $20 minimum wage in SF are not affected by $7.25 minimum wage

So we should raise the federal minimum wage so that so-called 1% of people can’t be ignored like you’re trying to do.

This is how our argument has looked to me:

You: “well the average is fine”

Me: “well the average doesn’t help those at the bottom”

You: “well they don’t matter to the average”

Your arguments need a lot more work. You just seem soulless with the points you’re trying to make.

deleted by creator

It’s a deliberately misleading chart, especially using median salary and mean productivity

deleted by creator

Yes, but the productivity is using the mean, not the median which is why that chart is flawed

I wonder what happens to this chart if you remove the top 1% from the calculations. “Median” basically means halfway between the top and bottom… The massive and increasing wealth gap means this graph is basically worthless.

If you remove 1% it will be showing the 51st percentile instead of the 50th…